Originally published at: Apple takes on banks with new 4.15% interest savings account | Boing Boing

…

1 Like

I’m not sure you can say they’re ‘taking on banks’ when they’re partnering with Goldman Sachs to provide the actual banking services.

18 Likes

I’m not keen on Apple-for-everything, though. Once they’ve got an addition to their walled garden, it’s only time before they leverage that payment advantage. I don’t see this ending particularly well for us.

16 Likes

If it sounds like its too good to be true it’s either a scam or there’s a catch. In this case i wonder what the catch is because i doubt Apple is doing this out of the goodness of their heart

10 Likes

My wife works in Bank Fraud and Anti-Money Laundering. Her employer recently opened a digital bank and offered an account with a 5% interest rate. The number of new accounts that were opened was huge, and so was the number of fraud alerts their system triggered. At one point it was over 20,000. I hope they have made allowance for this in their plans.

8 Likes

Are these accounts FDIC insured?

8 Likes

The “catch” seems to be:

- you have to be an apple card holder

- “cash-back” you earn from your apple card (Daily Cash?) must get deposited to your apple savings account

8 Likes

With rates going up, GS figures it’s worth paying a few points to hold onto those funds rather than pay them out.

2 Likes

A bit more info on the bandwagon here:

8 Likes

I think so. See footnote #3 on Apple’s press release.

4 Likes

Dang - maybe for my actual saving account I should consider something like that…

2 Likes

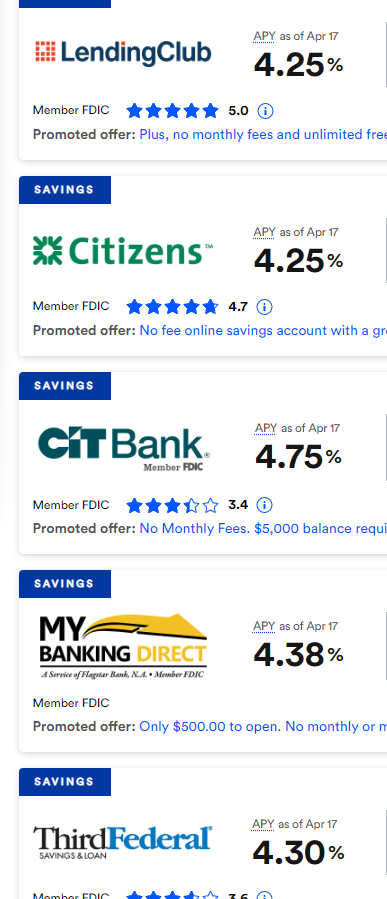

Of course, these rates are subject to change due to market conditions, which is why you used to be able to have 5%+ accounts and then suddenly you couldn’t do better than 1% when the fed slashed rates down to 0, and now that the fed is raising rates, you can now have 5%+ accounts again.

9 Likes

US savers get savvy ditching and switching banks

9 Likes

I chased rates a few years ago. Banks seems to trade off who has the best rate, get a bunch of new accounts, then let the rate drop and someone else has much better rates. It’s not work all the hassle IMHO. Just stick with one who tends to have relatively high rates. I’d be wary of having too much tied to a single company, like Apple.

2 Likes

You can get over 5% on US Treasury Bills right now. And there are definitely retail brokers that will let you buy and sell with no minimums and no fees.

6 Likes

Yep, that’s been the M.O. of my banks, for sure. Especially for Certificate of Deposits. They make it easy to open the new account but hard to transfer the money out after the first 6 months or whatever when they drop the rate back down to near zero. They give you a short window of time of about one week after it matures to get your money out before it automatically rolls over for another term.

Lately I’ve been using a different investment service that lets me buy CDs from a whole list of banks and automatically dumps the money back into my account when they mature, so hopefully I won’t have that situation moving forward.

3 Likes

I’ve been using Discover for my checking and savings for years. Savings APY is currently 3.75%. The rate is variable, but I think that even at it’s worst it hasn’t gone below 2%.

I don’t think it’s any more of a “catch” than Apple Card is (I’m a cardholder). There’s no fees ever, even if you miss your minimum payment, and low interest rates there, too. My best guess as to why this works for Apple is a whole hell of a lot of CC transactions for apple products are processed through the Apple Store and this way they probably save on those fees. It’s also awfully nice to have a second CC number just for online txns and you can rotate that number out with one tap - so that probably also heavily reduces fraud.

My guess is that this also benefits Apple in a similar way - maybe by not having to transfer apple cashback around? But I’m guessing like Apple card this is one of those things where the extra “benefit” to the consumer is justified by whatever the benefit is to Apple.

I’ve been using a no-fee online-only bank since I came to the US, and while they’ve been rock-solid (and supported me before I had any credit here!) I’ve been thinking about what to do about a high-interest savings account - maybe this is an option now. We’ll see.

8 Likes

Apple has a partner here, GS, but on its face, this sure does look like the first step of Apple’s move to financialization. I’m sure that @doctorow talks about this. This, and the enshitification that big tech tends to do.

4 Likes